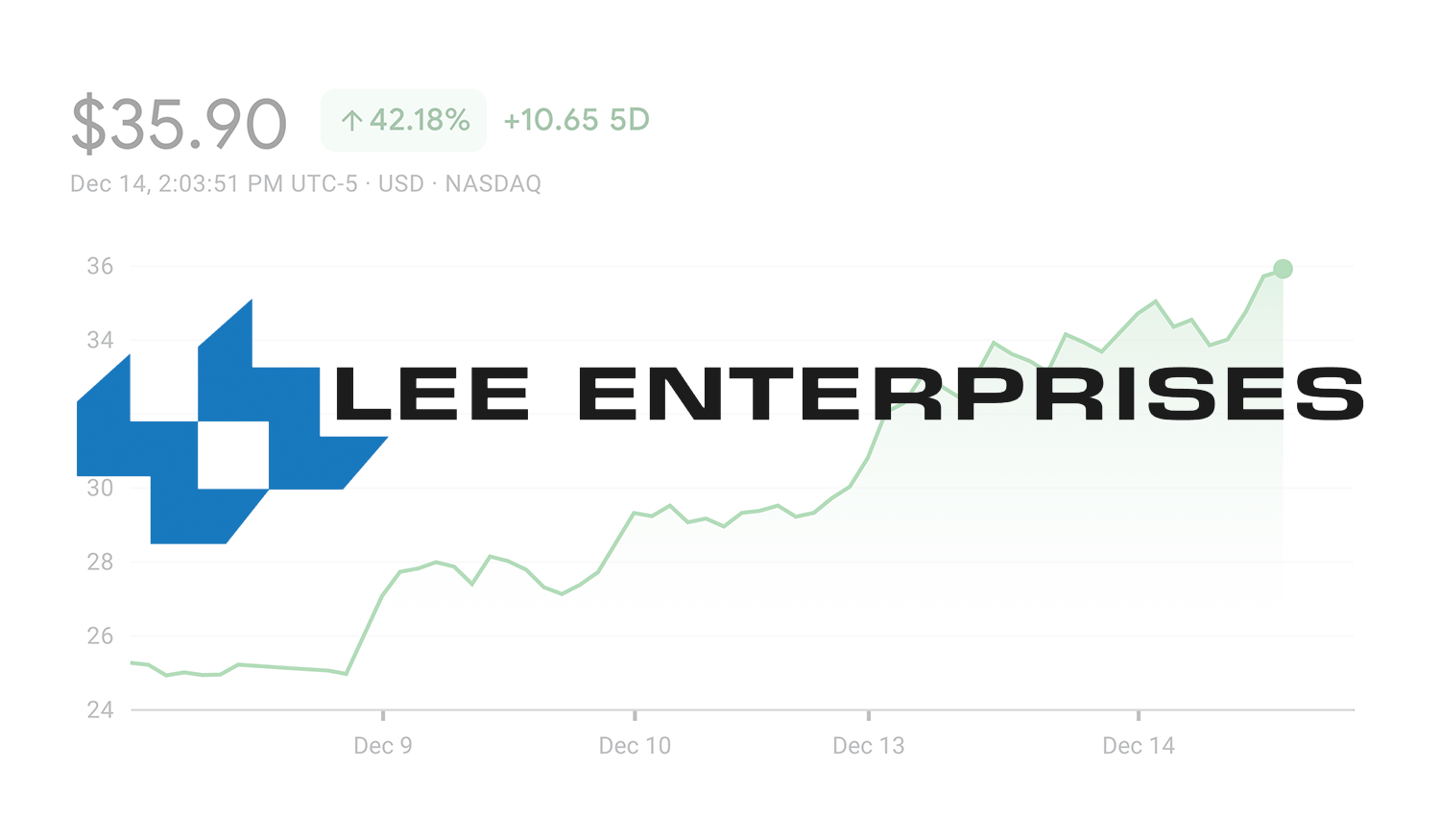

In a surprise development as Alden Global Capital pursues a hostile bid to acquire Lee Enterprises, Lee’s shares have shot up in value in the last week. The stock closed Tuesday at more than $36 a share.

Unless the trend reverses, that makes hedge fund Alden’s $24 a share offer a month ago — already rejected by Lee’s board of directors last week — dead in the water.

It now seems likely that Lee can remain independent and pursue its growth plans. An alternative scenario would be for Alden or another suitor to offer a much higher price.

How did Lee’s stock go so quickly from $18 a share before Alden’s bid to double that?

The company declined to comment, but two other investors I spoke with did. Given a strong financial report for the quarter ending in September and side businesses with strong growth potential, Lee had been undervalued.

Harris Kupperman, who represents two funds that he says own 7.3% of Lee’s stock, sent the Lee board a strongly worded letter saying, “Alden’s proposed purchase price is clearly insufficient and opportunistic, grossly undervaluing the business.”

“Their proposal comes precisely as (Lee’s) digital business transformation gains momentum,” the letter continued, “dramatically unlocking value for long-suffering shareholders.”

In an interview, Kupperman said that the low price a month ago reflects a longstanding negative investor bias against the industry. “Newspapers have performed pretty terribly for the past decade or more,” he said. “People don’t see what’s happening now.”

In his view, Wall Street took a closer look after the Alden bid and the strong earnings report and liked what it saw. Hence the rise to $34 a share.

Rapid digital growth is a particular strength, Kupperman said, with paid digital subscriptions up 50% year-to-year and digital revenues up 48%. The company now gets a third of its revenue from digital as print declines, he said, and it can increase that to half by 2023.

Kupperman suggested that a fair value for Lee’s stock would be $100 a share. The second investor I spoke with, who requested anonymity, put the value at a more conservative $50 to $55 a share.

He too said that Lee “is further along in digital transformation than people have realized.” He also pointed to the strength of the company’s other digital businesses, especially Town News, a content management platform with many clients beyond Lee’s own 77 papers.

In an annual report filed with the Securities and Exchange Commission Friday, Lee made a number of the same points about its growth prospects.

The filing also conceded that fending off Alden’s offer could be both expensive and a distraction to management. And it notes as another negative that Lee’s acquisition of Warren Buffett’s BH Media in March 2020 came just before the COVID-19 pandemic and ad downturn, slowing results it had hoped for.

Lee’s largest papers are the St. Louis Post-Dispatch and Arizona Daily Star in Tucson. The next three biggest all came with the BH acquisition — The Buffalo News, Omaha World-Herald and Richmond Times-Dispatch.

Buffett holds nearly all the company’s debt and may therefore have an influence on Lee’s management and board.

Nothing is certain once a company is thrown “into play” by a takeover offer. But the stock performance suggests that Lee newsrooms, worrying for the last month about deep cuts if Alden takes over, may instead have a relatively stable 2022 — especially if federal legislation subsidizing the salaries of local journalists comes through.

This article was updated to include Lee’s end-of-day stock price.