There has been plenty of speculation on who might buy Time magazine (and other news titles) from its new parent, lifestyle specialist Meredith.

The Koch Brothers? David Pecker's American Media, publisher of the National Enquirer? Tronc and its big-talking chairman, Michael Ferro?

But here is another possibility to consider — Meredith, having spent $1.8 billion to acquire all of Tiime Inc. in late November, might choose instead to keep several or all of the news magazines for itself.

A Time Inc. insider, requesting anonymity, pointed me to an indicator suggesting that keeping the combined company whole, with perhaps minor selloffs, is at least on the radar for Meredith chairman Stephen Lacy.

In an interview with the Wall Street Journal Feb. 15 and earlier, in a conference call with analysts Jan. 31, Lacy made much of the digital scale that the merger creates. He used the same figure both times: 170 million monthly unique visitors.

Digital ads sales is a numbers game, Lacy explained in the analysts call, and "this scale moves us solidly into the top 10 among U.S.-based companies as ranked by traffic, just behind Amazon and the Microsoft sites."

What remains unsaid, but highly relevant, is that the Time titles provide a much larger share of the digital traffic and digital ad revenue for the new Meredith, than do Meredith's pre-merger holdings.

Time, along with Fortune, Sports Illustrated and Entertainment Weekly, account for roughly 35 million of the 170 million, Meredith spokesman Art Slusark told me. Subtract those out and you are left with a less imposing 135 million and no top 10 ranking.

ComScore's basic report aggregates by magazine group rather than individual sites. The latest I can find, for January 2018, showed Meredith with 81.1 million and Time Inc. with 139.3 million monthly unique visitors.

Slusark declined to give me a title-by-title breakdown. But I found an alternative source, using a different metric.

For several years, the Magazine Publishers Association has been providing what it calls a "Media 360° brand audience report." Participating titles — and all of Time Inc.'s and Meredith's do participate — report in a standard format. The monthly spreadsheet shows the numbers of digital and print edition buyers, and separately, web, mobile and video audiences. Add them all up, and you have a total audience estimate. Duplication is likely, but the idea is that ad buyers have all the data they need for a combination that fits their needs.

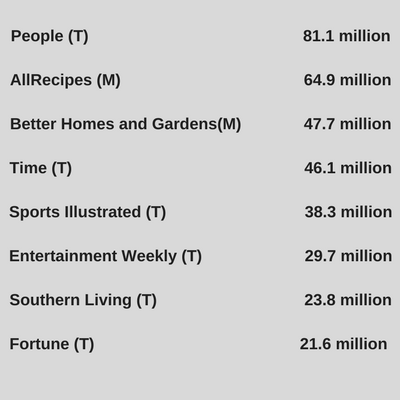

Top of the list for the merged company, provided by MPA research director Jeri Dack, is Time Inc.'s People — a sure keeper for Meredith, as it's America's most profitable title and the gem of the deal. But the order and numbers for other titles in the MPA's most recent report from December for total audience are eye-opening:

In other words, Time Inc. titles make up six of the top eight in the combined company. All four news titles are above 20 million per month.

The assumption that Meredith would probably sell the news titles is not without basis. The company extended itself financially to absorb the larger, but less healthy, Time Inc. Hence, a deal with Koch Equity to take a $650 million loan with a sweet payout — but no seats on the board or role in managing the magazines.

News magazine have never been in Meredith's wheelhouse. The company does not have editors specializing in that rhythm. However, plenty with those skills come along with the Time news titles, and Meredith could hire more.

The crux of the challenge from a business viewpoint is that Meredith's lifestyle content is more or less evergreen, creating audience and advertising opportunities well beyond the edition date. At news titles, it's the opposite — stories are perishable, often in the space of a week, sometimes, in the digital space, by the day.

Lacy touts the virtues of the lifestyle orientation in any presentation he gives — great loyalty and print renewal rates, opportunities to cross-sell readers and advertisers among related titles and sites, ease of moving young women readers on to different "life-stage activities, like having a child, or lifestyle activities, like cooking, gardening and decorating," as he told the Journal.

In the earnings call, Tom Harty, promoted to CEO that day, addressed the possibility of selling some Time titles directly (but in a keeping-our-options-open way):

"We'll explore divesting assets that are not core to our business and might perform better with a different owner. … We've been pleasantly surprised with recent transaction prices in the media space, and inbound interest for certain properties has been strong."

The call included a wealth of added detail, worth exploring for those truly interested, like Time employees nibbling their knuckles, trying to figure what's next. In a nutshell, Lacy and company were highly complimentary of the Time brands, and by implication, their editorial quality and audience appeal.

However Harty turned brutally blunt in saying that a new ad sales strategy over the past two years at Time Inc. proved to be a disaster:

"Historically, Time Inc., which owns the best portfolio of media assets in the industry, outpaced industry performance. However, in 2016, Time Inc. realigned its sales structure and its go-to-market strategy to focus on advertising categories instead of their individual media brands. This has resulted in revenue declines much steeper than both our own or average industry performance."

Print advertising revenue losses, for instance, were running well over 20 percent late in 2017, he said. Profitability in both print and digital operations had fallen below not just Meredith's but the industry average.

Those problems may take a year or two to work through, Harty continued, but they are fixable.

To be clear, I'm not saying that Time will end up as part of Meredith, rather that it plausibly might. My Time friends would much prefer that outcome to life with some of the potential buyers such as Pecker, whose willingness to buy rights to, then kill, the story of one of President Trump's sex abuse accusers has come under sharp scrutiny.

Meredith probably has a fiduciary responsibility at least to consider a premium offer for Time regardless of the source. Think Sheldon Adelson's family paying Gatehouse 40 percent more in late 2015 for the Las Vegas Review Journal than Gatehouse had paid to acquire it and seven smaller papers seven months earlier.

Spokesman Slusark points out that Meredith took control only a month ago and still has a lot to learn beyond the info used to close the deal, now that its own executives and managers can dive into operating details. That could influence decisions to sell or keep.

Consider, though, these potential signals that Meredith is in it for the long run:

- Lacy, a super salesman among other skills, has chosen to talk up the virtues of the merger to the investment community, rather than take the more cautious route of waiting until later when integration of the two operations is further along.

- He is under no obligation to use the 170 million unique visitors figure for the combined company but has done so repeatedly.

- Meredith sold Time Inc. UK, a collection of 57 European titles, on Feb. 26 for a reported $175 million. That goes some distance to easing the pain of aggressive borrowing to complete the acquisition.

- Finally I noticed that on the day the merged operation took place, workers at Time Inc.'s New York City headquarters were greeted by signage that had been changed overnight to Meredith. Lacy and Harty were shaking hands in the lobby.

That hints at a successful and ambitious company, for now the nation's largest magazine publisher, thinking it can grow its rebranded beachhead in Manhattan, rather than falling back to a lifestyle comfort zone at its heartland Des Moines headquarters.