Covering COVID-19 is a daily Poynter briefing about journalism and coronavirus, written by senior faculty Al Tompkins. Sign up here to have it delivered to your inbox every weekday morning.

Covering COVID-19 is a daily Poynter briefing about journalism and coronavirus, written by senior faculty Al Tompkins. Sign up here to have it delivered to your inbox every weekday morning.

Let’s say you owe the bank money. Maybe you are behind on a loan, for example. Then the stimulus check arrives in your checking account. It turns out Congress allowed banks to grab the money to pay any debts you owe them before you ever spend a dime of it.

Or, let’s say a person has overdraft charges left behind on an account they thought was closed. The bank could pay itself before posting the stimulus deposit.

The American Prospect got ahold of audio from a webinar with the Treasury Department and banking officials that occurred last week. Here’s what it found:

Ronda Kent, chief disbursing officer with Treasury’s Bureau of the Fiscal Service, can be heard explaining that banks had posed questions to her about “whether these payments could be subject to collection from the bank to which the money is deposited, if the payee owes an outstanding loan or other payments to the bank.” She responded — twice — that “there’s nothing in the law that precludes that action,” while counseling that the banks’ compliance officers should consult with their legal offices about what policies their banks will implement. “You will want to know for your bank what your bank has decided to do,” Kent said.

You can listen to the audio here. First, Kent explains how the IRS will not pass along stimulus payments to people who are behind on child-support payments. Then, at 3:26 on the recording, she talks about banks keeping the money to pay debts.

Late Thursday, USAA announced it would not collect stimulus funds to pay for overdraft fees. USAA says it is pausing overdraft collections for 90 days. Other big banks including JP Morgan Chase, Bank of America and Wells Fargo also said they won’t try to grab the stimulus checks to pay for negative account balances.

By the way, if a creditor has a court-ordered “garnishment” on a person’s wages, the debt collector may be able to grab that person’s stimulus money, too.

The cost of lost conventions

Municipal bonds, a staple for conservative investors, may suddenly be rated lower as cities watch conventions evaporate just at the beginning of the summer conventions season.

Hotel taxes are a key source of the money that pays for the convention centers that cities have built and expanded across the country. Empty hotels don’t produce tax revenue, and even a “flattening curve” does not fill hotels when businesses might take months to recover from months of being shut down.

The Center for Exhibition Industry Research in Dallas said 80% of the 2,500 business-related conventions that would have been held between the beginning of March and the middle of May in the U.S. were canceled. By one estimate, it could amount to a $22 billion loss of business. The 20% that survived were those that squeaked through the first week or so of March.

The trade show industry in America includes 9,400 conventions a year, and that is just “business-to-business” gatherings, sort of like what journalists might attend. Add to that number home, garden and food shows, among others, that the public might attend.

Take, as an example, just four conventions you probably have never heard of:

- Inspired Home Show by the International Housewares Association (Chicago)

- Healthcare Information and Management Systems Society Global Health Conference and Exhibition (Orlando)

- Affordable Shopping Destination Market Week (Las Vegas)

- Natural Products Expo West (Anaheim)

By my calculation, just those four conventions involved more than 2.5 million net square feet of convention hall space. That is equal to about 50 football fields. Put another way, the average square footage of a typical American Walmart store is 105,000 square feet, so it’s about two dozen Walmarts stuck together. Now, expand to include the full list of canceled conventions from March to May and you start to see the real impact.

A Center for Exhibition Research economist said:

Our estimates show that this would result in a loss of 41 to 65 million (net square feet) and $2.3 billion to $3.6 billion in show organizer revenue. Combined with direct spending by exhibitors and attendees, the total loss to the economy would be $14 billion to $22 billion.

Gasoline tax income is drying up

A week ago we talked about how insurance companies are giving out auto insurance rebates because we are driving so much less, and crashing less as well. But then there is a cost, too.

When we drive less, we use less gasoline. And that means we pay less fuel tax, and I mean a lot of fuel tax.

Overall traffic is down around 40% according to INRIX, a traffic data analytics company.

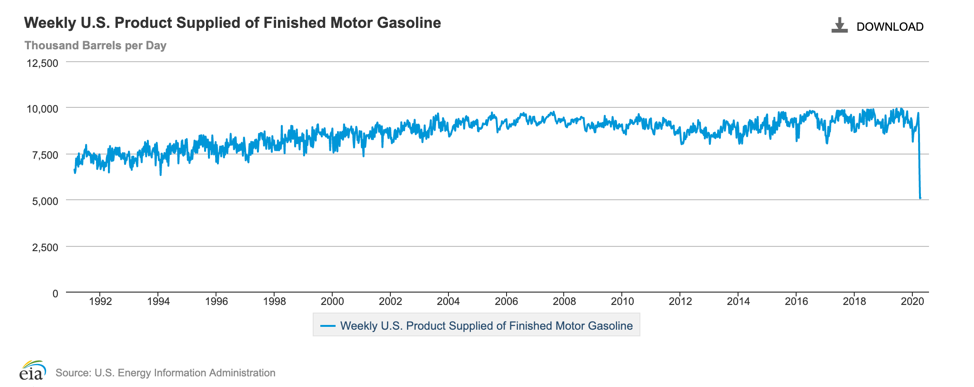

And how much less fuel are we using as a result? Look at this chart from the Department of Energy. Notice the trend from left to right. Then the chart drops off a cliff. In just one week, the week that ended March 27, gasoline consumption dropped by nearly one-third to a 25-year low.

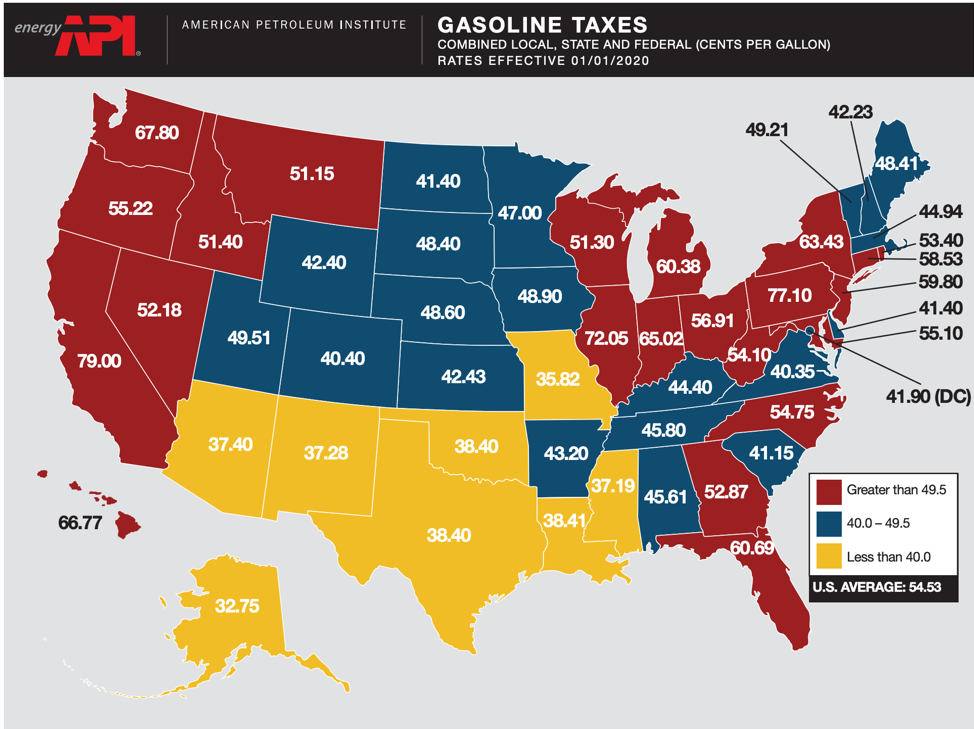

There are two main taxes on fuel. One is federal and the other is a state gasoline/diesel tax. The federal gasoline tax is 18.4 cents per gallon. The $44 billion or so total that states take in from fuel taxes makes up the backbone of their transportation budgets, the funds that pay for roads and bridges.

There are two main taxes on fuel. One is federal and the other is a state gasoline/diesel tax. The federal gasoline tax is 18.4 cents per gallon. The $44 billion or so total that states take in from fuel taxes makes up the backbone of their transportation budgets, the funds that pay for roads and bridges.

But states add more. In some cases, a lot more. Pennsylvania, for example, charges 57 cents a gallon in gasoline taxes. The American Petroleum Institute has a map of what you pay when you combine the federal 18.4 cent tax with the taxes that state and local governments impose. You start to see why you pay so much more for fuel in California, Pennsylvania and Illinois and less in oil-producing states like Texas and Oklahoma. Missouri and Alaska have the lowest combined tax rates on gasoline.

OK, stay with me here because there are a couple of stories in this thread.

OK, stay with me here because there are a couple of stories in this thread.

Most states base the fuel tax on each gallon. When gas prices were higher, states loved to tax fuel as a percentage of the price of a gallon. But, as prices went up and down, states saw the unreliability of basing the tax on a percentage of the price. Nationwide, the federal government said, gasoline prices are down 98 cents per gallon (on average) from a year ago.

States are watching all of this closely. North Carolina, for example, said more than half of the state’s Department of Transportation revenue comes from fuel taxes (21% comes from car sales, which are also way down) and the state is scrambling to find ways to quickly cut spending — likely in planned projects because they can’t just stop projects that are already underway. North Carolina depends more on fuel revenues for department of transportation projects than any other state, according to the Tax Foundation.

Overall, as fuel gets cheaper, tax income drops. And as we use less fuel, tax income drops, too. A double whammy.

Nationwide, 20 cents out of every dollar you spend on gasoline goes to taxes.

Exercise equipment is a hot commodity

Exercise equipment is a hot commodity

You know what is selling fast these days? Exercise equipment, which is soon to be laundry hangers, I expect.

Adobe’s Digital Economy Index, “which analyzes trillions of online transactions across 100 million product SKUs in 18 product categories,” said fitness equipment sales have surged since the COVID-19 pandemic. The report said:

With many U.S. consumers confined to their homes starting in March, orders for fitness equipment (kettlebells, dumbbells, stationary bikes and treadmills) has increased 55% in online sales.

Nautilus, a company that makes fitness equipment, issued a sales forecast last week. Reuters reported:

Nautilus said it expects first-quarter net sales to rise 11% from a year earlier to $94 million, the first increase in more than a year, as people turn to at-home exercise equipment because of restrictions on movement.

“Demand for many of our home-fitness products continues to outpace supply and we are pulling all levers to accelerate the manufacturing and delivery of key products,” Chief Executive Officer Jim Barr said.

Peloton stock is also way up since mid-March. Peleton reported that downloads of its app are five times higher than in February. Part of that may be attributable to the company’s 90-day free trial offer during the COVID-19 stay-at-home orders.

Some gyms, shut down by the virus, have turned to renting out some of their equipment.

Pawnshops will be busy

With 17 million people out of work, America’s pawnshops will be a lifeline for a lot of folks who need money to pay rent and buy food.

We can see this coming by looking to the East. Thailand, for example, saw a rush to pawn shops as soon as they were allowed to reopen.

Florida has already declared pawnshops “essential” and allowed them to stay open.

The pawn industry is way bigger than you might think. McClatchy reported that the pawn business has been soft because the economy was solid:

The industry research group IBIS World estimated that the size of the pawn industry nationally is $5.8 billion for 2020, employing more than 41,000 people across nearly 12,000 businesses. Pawnshops have slid over the past five years as the economy grew steadily and gold prices fell.

IBIS World said from 2013-2018 the pawn industry declined by a percentage point even as the economy roared.

Usually, about three-quarters of pawnshop borrowers pay off their loans and get the stuff that they put up as collateral back. But, McClatchy reported, even in good times, there are some Americans who you might call “unbanked.” For them, pawnshops are their banking system:

Pawnshops often serve a segment of the population that’s called the unbanked — people without a checking account or who cannot qualify for a credit card. They tend to operate in poorer areas and can be polemic. Some consumer groups view the business model as usury while those in the business argue they act as a lender of last resort.

The unbanked are a segment unlikely to get direct help from the stimulus efforts that are expected to help get cash in the hands of workers. That’s why consumer advocacy groups are asking the federal government, as part of stimulus efforts, to extend to all consumers the protections given to military service members against predatory lending rates and to reach the unbanked and lower-income workers whose jobs might not come back or will take longer to return.

The Federal Deposit Insurance Corporation, which insures banks, said 25% of people in America qualify as “unbanked” or at least “underbanked.” The FDIC said:

Estimates from the 2017 survey indicate that 6.5% of households in the United States were unbanked in 2017. This proportion represents approximately 8.4 million households. An additional 18.7% of U.S. households (24.2 million) were underbanked, meaning that the household had a checking or savings account but also obtained financial products and services outside of the banking system.

PawnGuru tried to figure out what people pawn when they need cash and found that the answer depends on the part of the country they are in. In southern and western states, guns are way more popular at pawn shops. In Colorado and Florida, people pawn a lot of vehicles. Jewelry accounts for about 5% of pawns, tools about 8% and antiques about 9%. A third of all pawns involve electronics. Apple products are by far the most popular for pawn shop buyers. Diamond rings lose a lot of value when they are pawned.

Most jewelry is pawned by women. Most guns are pawned by men.

PawnGuru reported:

It turns out that weapons serve as a remarkably durable store of value. While electronics dominate pawnshop inventories, they depreciate much faster than firearms do. That’s because obsolescence is a much smaller factor in the weapons market. A non-Apple laptop or a smartphone is as good as dead after 5 years. Even an Apple has very little value after a decade. But guns don’t change radically every three years, which means they hold value for a long time.

PawnGuru also found:

Luxury watches are popular in Long Island, Miami and Los Angeles. Designer clothes and bags win out in Dallas and San Francisco. And guns over-index in popularity in a tremendous number of cities; Atlanta, Birmingham, Houston, Jacksonville, Kansas City, Midland, Montgomery, Nashville, Oklahoma City, and Phoenix all count guns as their most disproportionately popular item for pawning.

The Washington Post profiled a pawn shop in Ash Flat, Arkansas, that really put the unfolding desperation into context:

Pawnshops allow people with few alternatives to borrow against their possessions. In Ash Flat, where the median household income of $19,837 is less than one third of the national average, it can be the only option. Pawning a generator for $300 could cover a car payment. A 12-gauge shotgun might command $100, and provide a cushion until Social Security comes through.

Dr. Fauci, the love doctor

Dr. Anthony Fauci sounded more like Dr. Ruth Thursday morning when Good Luck America (a Snapchat show) asked him if it would be safe for people to hook up with Tinder prospects in the midst of a pandemic. Fauci, and you have to give him credit for turning to unorthodox messaging channels to reach every audience he can, didn’t flinch at the question. He said it is tough, “Because that’s what’s called relative risk.”

Then he went on teaching, saying that it will not be enough to just ask a person if they are feeling sick, because so many COVID-19 infected people do not show symptoms of the virus.

Did doctors really wear masks like this?

If you use the word “doctor” loosely, the answer is yes — during the plague in the 17th century.

If you use the word “doctor” loosely, the answer is yes — during the plague in the 17th century.

Erin Blakemore at National Geographic mined up this wonderful history lesson.

The story said, “Plague doctors filled their masks with theriac, a compound of more than 55 herbs and other components like viper flesh powder, cinnamon, myrrh, and honey.”

A leading “expert” at the time thought the bird-like beak would create space for the herbs to do whatever they were supposed to do before the “toxic air” entered the person wearing the mask. It is unknown how many people died from having the bejeebers scared out of them when approached by a doctor who looked like a giant raven.

This might be an opportunity for you to explore all of the homespun ways that people are “fighting” the coronavirus. I have a friend who just washed her refrigerator inside and out. People are scrubbing every darn thing.

I have seen no evidence of anybody getting the virus from a fridge, but hey, why not? It probably needed cleaning.

We’ll be back Monday with a new edition of Covering COVID-19. Sign up here to get it delivered right to your inbox.

Al Tompkins is senior faculty at Poynter. He can be reached at atompkins@poynter.org or on Twitter, @atompkins.